In 2026, usage-based pricing (UBP) is no longer an emerging trend or a niche choice made by API-first infrastructure companies. It is becoming the dominant commercial model in software, accelerated by the rise of AI-powered products, the structural shift in how software delivers value, and mounting pressure from enterprise buyers who are tired of paying for seats that go unused.

Flexible Pricing

For most of the last decade, SaaS pricing followed a simple, predictable formula: pick a tier, pay a flat monthly fee, add seats as the team grows. It was easy to budget, easy to sell, and easy to understand. It was also, increasingly, misaligned with how software actually creates value, and the industry has spent the last two years correcting that misalignment at speed.

In 2026, usage-based pricing (UBP) is no longer an emerging trend or a niche choice made by API-first infrastructure companies. It is becoming the dominant commercial model in software, accelerated by the rise of AI-powered products, the structural shift in how software delivers value, and mounting pressure from enterprise buyers who are tired of paying for seats that go unused.

For founders building SaaS products today, understanding this shift is not optional, the pricing model you choose will directly affect your growth rate, your net dollar retention, and your ability to raise capital.

What usage-based pricing actually means

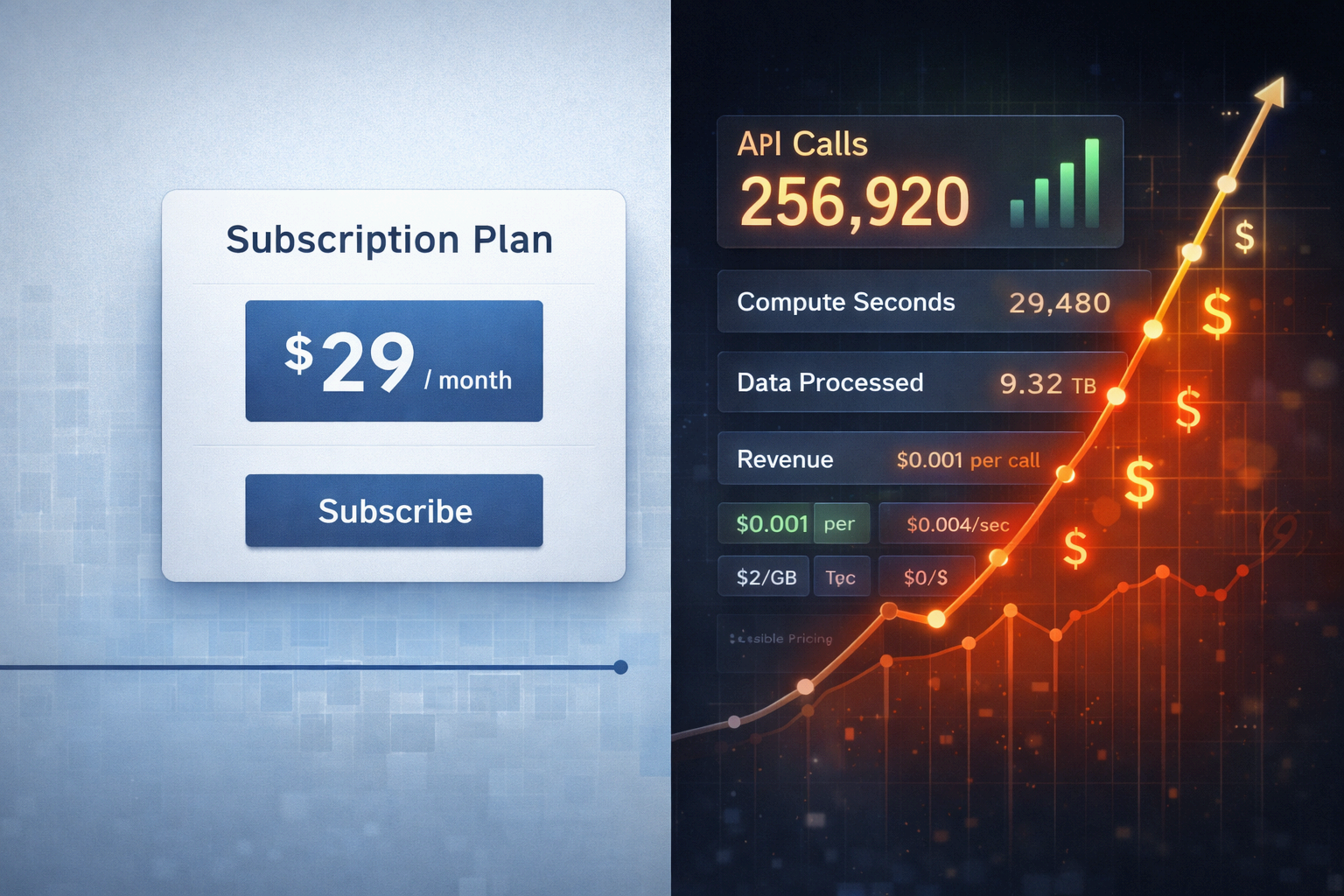

Usage-based pricing, also called consumption-based pricing, is a model in which customers are charged based on how much of a product they actually use rather than paying a fixed subscription fee regardless of consumption.

The billing metric varies by product: it might be API calls, tokens processed, compute hours, active sessions, data volume, transactions completed, or any other measurable unit of output that tracks the value a customer receives.

This is distinct from traditional per-seat or tiered subscription pricing, where a company pays the same amount every month whether its team uses the tool heavily or barely at all. It is also distinct from outcome-based pricing, a newer and more nascent model where the vendor charges based on measurable business results delivered, per ticket resolved, per lead converted, per contract analyzed, rather than on consumption of the product itself.

The practical difference matters enormously for how both vendors and buyers think about the cost of software.

The data behind the shift

The clearest picture of how rapidly this transition is happening comes from Zylo's 2026 SaaS Management Index, which is built on analysis of more than 40 million real SaaS licenses and over $75 billion in spend under management, making it the most grounded annual benchmark available on SaaS economics. Its findings for 2026 are striking.

Average enterprise SaaS spend rose 8% year-over-year despite the total number of applications remaining essentially flat at around 305 per organization. The growth is not coming from more software. It is coming from how that software is priced.

On the vendor side, Metronome (now part of Stripe following its 2025 acquisition) surveyed 100 SaaS companies for its State of Usage-Based Pricing 2025 report and found that 78% of companies currently using UBP adopted it within the last five years, with nearly 50% doing so in the last two years alone.

OpenView Partners, whose annual SaaS Benchmarks Reports have tracked this model since 2021, reports that 38% of SaaS companies now use some form of usage-based pricing, up from 27% in 2023, and companies with primarily consumption-based models grew revenue approximately 8 percentage points faster on average than those on flat-rate subscription models.

The enterprise data reinforces the trend from the buy side. Metronome's survey found that 77% of the largest software companies have incorporated consumption-based pricing into their revenue models.

OpenView's research shows that 61% of SaaS companies now leverage some form of hybrid pricing combining a base subscription with usage-based components, a structure that has emerged as the pragmatic middle ground between full consumption billing and flat-rate subscriptions.

Why AI broke the per-seat model

The acceleration of usage-based pricing in 2025 and 2026 is impossible to separate from the mass integration of AI features into SaaS products. The economics of AI-powered software are fundamentally incompatible with the per-seat model, and this incompatibility is forcing a rethink of pricing architecture across the entire industry.

A traditional SaaS product, a CRM, a project management tool, a design platform, has near-zero marginal cost per additional user. Serving one more seat costs essentially nothing, which is why per-seat pricing worked well as a growth model: you added users, revenue scaled, margins held.

An AI feature that calls a large language model has real per-request compute costs that can vary significantly depending on the complexity of the input. The underlying infrastructure cost is tied to consumption, not to headcount. Building a flat-rate subscription on top of that cost structure creates a misalignment between what the vendor spends to deliver the product and what the customer pays to use it.

This is precisely why major SaaS incumbents have been restructuring their AI pricing in the open. Salesforce introduced Flex Credits for its AI capabilities. Microsoft built Copilot Credits into its M365 stack. Adobe deployed a generative credit system across Creative Cloud. These are not minor feature updates, they represent a deliberate pivot by some of the largest software companies in the world toward consumption-linked cost structures for AI-powered functionality.

High Alpha's 2025 SaaS Benchmarks Report found that 41% of SaaS companies with AI features are formally monetizing them, with 25% using usage-based pricing and 22% using a hybrid model. These numbers will rise sharply. AI is also driving spending volatility that buyers can no longer ignore: Zylo's 2026 index found that spending on AI-native applications surged 108% year-over-year overall, and by 393% among organizations with more than 10,000 employees.

The buyer problem: unpredictability is real

The shift to usage-based pricing is not without friction. The same Zylo data that shows explosive AI spend growth also documents the pain it is creating for enterprise buyers. In a survey of 218 IT leaders conducted for the 2026 SaaS Management Index, 78% reported experiencing unexpected charges tied to AI features or consumption-based pricing in the past 12 months. A further 61% said they had been forced to cut projects or reduce scope due to unplanned SaaS cost increases.

Business units now control 81% of SaaS spend while IT directly manages just 15%, which means that AI tools and consumption-based products are entering organizations faster than governance structures can adapt. Expensed SaaS purchasing, employees buying tools with corporate cards without going through IT procurement, grew 267% year-over-year in the 2026 index. ChatGPT is now the most commonly expensed application in enterprise environments.

For SaaS founders, this buyer-side tension is a product design problem as much as it is a pricing problem. Customers want consumption-based pricing for its alignment with value, but they also need cost predictability for budgeting. The vendors who are winning in this environment are those who solve both sides of the equation: they charge based on usage, but they give customers granular visibility into what is being consumed, where costs are accumulating, and what guardrails are available to prevent surprise overages.

What the hybrid model actually looks like

The structural solution that the market has converged on is the hybrid pricing model: a baseline platform fee that covers a committed level of usage or a minimum set of features, combined with usage-based billing for consumption above that threshold. This structure gives vendors predictable base revenue while creating a natural expansion mechanism as customers use more. It gives buyers a budget anchor while preserving the flexibility to scale usage up or down.

OpenView's data shows 61% of SaaS companies already deploy some form of hybrid model. Chargebee's 2025 State of Subscriptions Report found that 43% of companies are now on hybrid structures, with adoption projected to reach 61% by the end of 2026. IDC has forecast that 70% of software vendors will refactor their pricing away from pure per-seat models by 2028.

The companies that have executed this transition well, Datadog, Snowflake, Twilio, and increasingly OpenAI at the API level, share a common characteristic: they chose a billing metric that maps directly and obviously to the value a customer receives from the product.

- Snowflake charges for compute credits consumed.

- Twilio charges per message or per minute.

- Datadog charges based on the volume of infrastructure being monitored.

In each case, the unit of billing is also the unit of value, which means revenue grows automatically as customers succeed with the product, without requiring manual upsell motions or contract renegotiations.

The founder decision: how to choose the right model

For a founder building a SaaS product in 2026, the pricing decision is one of the highest-leverage choices in the business. Research from Simon-Kucher & Partners, the pricing consultancy, estimates an average revenue lift of 32% when SaaS companies systematically address pricing, compared to 15% from new customer acquisition and 10% from product improvements. Despite this, the average SaaS company spends approximately 8 hours total on pricing over the entire life of the business, according to ProfitWell data.

The starting point is identifying the right value metric

The unit of consumption that most closely tracks the value your product delivers to customers. This is not always obvious, and getting it wrong is expensive.

Mixpanel famously had to change its billing metric from raw events to tracked users after discovering that raw events created a misalignment between price and perceived value. The right metric is the one your customers are actively trying to maximize; if you align price to that metric, revenue scales with customer success rather than fighting it.

A few practical principles apply regardless of product category

Freemium or low-friction entry still makes sense at early stages, remove barriers to adoption before worrying about expansion mechanics. Usage or credit components should be introduced for features where consumption is genuinely variable and infrastructure costs scale accordingly.

For enterprise buyers, a committed baseline fee removes the budgeting anxiety that drives churn on pure consumption models. And pricing should be revisited on a regular cadence, Bessemer Venture Partners recommends every six months, because the market, the cost structure, and customer willingness to pay all change faster than most founders assume.

The pricing model is also a signal to investors

Metronome's data shows that forward-thinking investors view usage-based metrics as evidence of product adoption, performance, and virality, all of which are harder to fake than seat counts. Net dollar retention, the metric that measures revenue expansion from existing customers, is consistently higher for companies on hybrid and consumption-based models than for those on flat-rate subscriptions. OpenView's data shows a +14% median improvement in net dollar retention following a well-executed pricing and packaging change.

The outlook for 2026 and beyond

The direction of travel is clear. Gartner projects global software spending will reach $1.43 trillion in 2026. That spending is increasingly structured around consumption, value alignment, and AI-linked billing, not headcount. The next frontier is outcome-based pricing, where vendors charge for results rather than usage.

Gartner projected that over 30% of enterprise SaaS solutions would incorporate outcome-based components by 2025, and that number is growing as AI agents make it easier to measure and attribute business outcomes directly to software actions.

For SaaS founders, the window to build consumption-aligned pricing architecture into a product from the beginning is right now. Retrofitting a per-seat model into a hybrid or usage-based structure after the fact is painful; it requires renegotiating existing contracts, rebuilding billing infrastructure, and managing customer expectations through a transition.

Companies that get the pricing model right at the foundation have a structural advantage that compounds over time, both in growth rate and in the quality of the investor conversations they are able to have.

The flat-rate subscription is not disappearing. For products where usage is predictable, value accrues per user, and the cost structure is flat, it remains the simplest and most defensible model.

But for any product where AI is central, where usage varies meaningfully across the customer base, or where the value delivered scales with consumption rather than with headcount, the market has moved. Building a per-seat model on top of an AI-powered product in 2026 is not a conservative choice, it is a bet against the direction of the entire industry.

Resources

- Zylo, "2026 SaaS Management Index": zylo.com

- Metronome / Stripe, "State of Usage-Based Pricing 2025": metronome.com

- OpenView Partners, "Usage-Based Pricing Research Hub": openviewpartners.com

- High Alpha, "2025 SaaS Benchmarks Report": highalpha.com

- Zylo, "SaaS Predictions for 2026: A Shift in Spend and Governance": zylo.com

- Zylo, "Usage-Based Pricing vs Subscription": zylo.com

- Chargebee, "Usage-Based Pricing for Growth in a Changing Landscape": chargebee.com